This Article is written by Gerry Bosco, one of Australia’s leading mortgage brokers assisting more borrowers get approved in the face of changing lending conditions. Need help with borrowing for your next home or investment? Call Gerry today on 1300 739 161.

What are average monthly living expenses?

Living expenses play a potentially crucial role in a lender’s servicing calculator. They are generally one part of the serviceability calculator that cannot really be reduced past a minimum floor, but certainly does have the potential to go much higher if applicants declare more than the minimum as specified by each specific lender as generally lenders will take the higher of the two.

What is the Household Expenditure Measure or HEM?

A particular method of calculating an applicant’s living expenses has been implemented almost across the board in recent times (estimated to be 70-80% of lenders). This method is called the Household Expenditure Measure (HEM). The HEM is a benchmark lenders use in an attempt to estimate a loan applicant’s annual living expenses — this forms part of the overall outgoing figure which in turn makes up part of the calculation that determines borrowing capacity. It was developed by using local survey data, is also linked to CPI and factors in the type of household.

There are several elements of the HEM which make up the estimated figure for any given applicant. These are:

- The city/state in which the borrower lives – e.g. – Sydney & Melbourne are considered to have higher living expenses compared to the other cities around Australia. Internationally these two cites are in comparison with some of the most expensive cities in the world such as Dubai and London.

- Household type – single, couple, family etc.

- The number of dependent children;

- Lifestyle expenses based on overall spending which is categorised into:

a) Absolute basics – food, utilities, transport, communication etc.

b) Discretionary basics – take-away food, restaurants, alcohol, entertainment etc.

c) Discretionary non-basics – overseas holiday, house cleaner, luxury items etc.

In simple terms, the purpose of using the HEM is like using lesser used methods such as the HPI (Henderson Poverty Index – which focused on minimum income requirements relative to living costs) in that it assists lenders in make sure they are complying under the National Consumer Credit Protection Act 2009 (NCCP) by taking reasonable steps in determining whether or not a borrower can comfortably afford their loan repayments.

How Does Income Affect HEM?

Generally speaking, household income levels have a direct influence on the minimum living expenses calculated figure. Most lenders have a different weighting to how income affects the overall HEM estimate so it is difficult to quantify this across the board. It should also be noted that most lenders also add a non-disclosed buffer over the minimum HEM based on their risk appetite at the time which can be adjusted as their appetite changes.

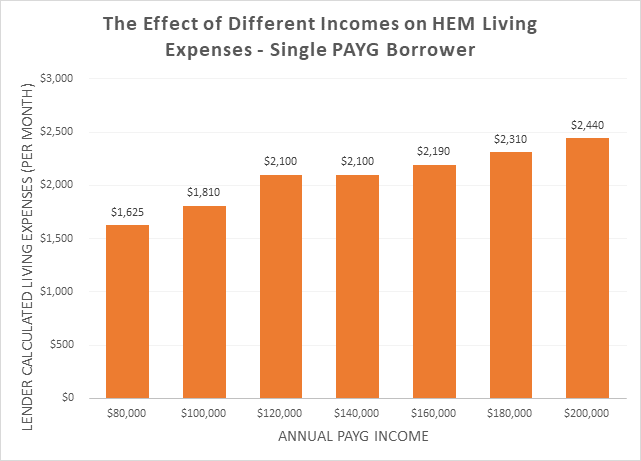

In the below example, we will illustrate how the HEM figures positively correlate with income as it increases. We have used a simple single applicant on varying incomes using a major lender’s servicing calculator. Everything else relating to the serviceability calculator is disregarded for the purpose of this illustration.

As can be seen above, there is an obvious positive correlation between income and the lenders calculation of living expenses – as income increases, so do the living expenses. There is a comparatively steep jump from $100,000 – $120,000 & an odd pause in the increase at the $120,000 – $140,000 level for unknown reasons. We also noticed there was a max out to the increasing living expenses. When income reached approximately $240,000, living expenses stopped at about $3,170 per month. Any income above this level did not see an automatic minimum increase in living expenses.

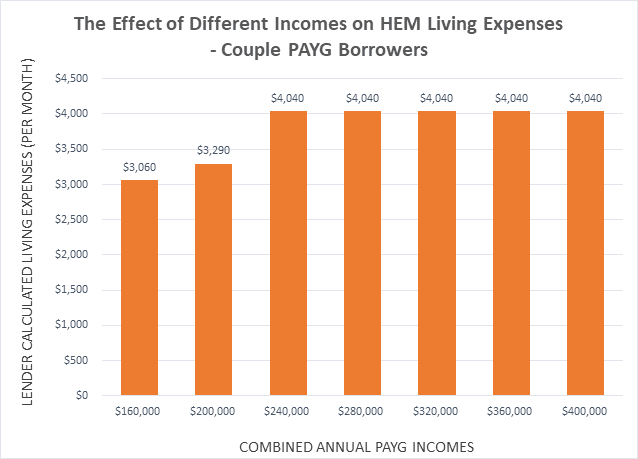

In another example, we will show a similar scenario but this time we will use a PAYG couple each earning full time salaries.

Here we can see a sharp increase between $200,000 – $240,000 then there is a plateau effect at the $240,000 level where no matter how much more income is earnt, the lender calculated minimum living expenses does not increase past this point.

As a reminder, it should be noted that although both examples show that after a certain income level, the lender calculated minimum living expenses do not increase – this does not mean in absolute terms that living expenses hit a ceiling. Living expenses do not have a maximum limit when declared by the borrower(s). Lenders will almost always take the higher of the two between their minimum as calculated and the borrowers’ declared amount.

What’s Next?

There is also a more recent trend perhaps in response to regulator intervention and the influence of the Royal Commission findings thus far, which is seeing lenders asking for specific breakdown of each expense category for borrowers by providing a borrower declaration or statement. This is likely the beginning of a new phase in highly scrutinised living expenses by the lenders. We have started to see more and more lenders requesting bank statements for the purpose of checking transactions that can be matched with the declared expenses.

These systems are also being automated by lenders and 3rd parties who have been increasingly investing in software for the purpose of data matching and the auto categorisation of living expenses. This technology is being used already by some major lenders in their websites & phone applications.

These changes to living expenses are having a flow-on impact into borrowing capacity calculations for borrowers – with these changes we’re likely to see more borrowers having to use products such as bridging loans to support them when upgrading their homes before selling etc.

Although not perfected quite yet, it would seem like this is the way of the future as the technology becomes more refined and as the most efficient method of tracking and evidencing living expenses.

Are you looking for a bridging? Speak with one of our experienced Sydney based finance brokers today.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment

You must be logged in to post a comment.