Afterpay is the latest payment option for consumers to use instore and online.

Afterpay’s motto is, Shop Now. Enjoy Now. Pay Later. In Four Simple Instalments, but is it really that simple and more importantly how will this impact your spending habits and personal budget?

This is NOT a product endorsement or recommendation to use the product, this blog is operational review based on the facts that are available at the time of writing, with a clearly disclosed opinion considering how Afterpay compares with using a credit card to make a purchase – blog intended to entertain – ENJOY!

How Does Afterpay Work?

Afterpay is another way for a consumer to pay either online, or instore.

- Merchants offer Afterpay to end-customers with a BUY NOW, PAY LATER offer

- End-customers pay for items in 4 fortnightly instalments

- Afterpay does not charge customers any interest, establishment or monthly fees

- After the initial Afterpay signup no additional information required at checkout

- Afterpay pays merchants upfront (less Afterpay fee)

- Afterpay retrieves funds from the consumer

Afterpay makes money by charging:

– Retailers a fee for use of the Afterpay payment platform

– Customers late fees if they don’t pay their instalments on time.

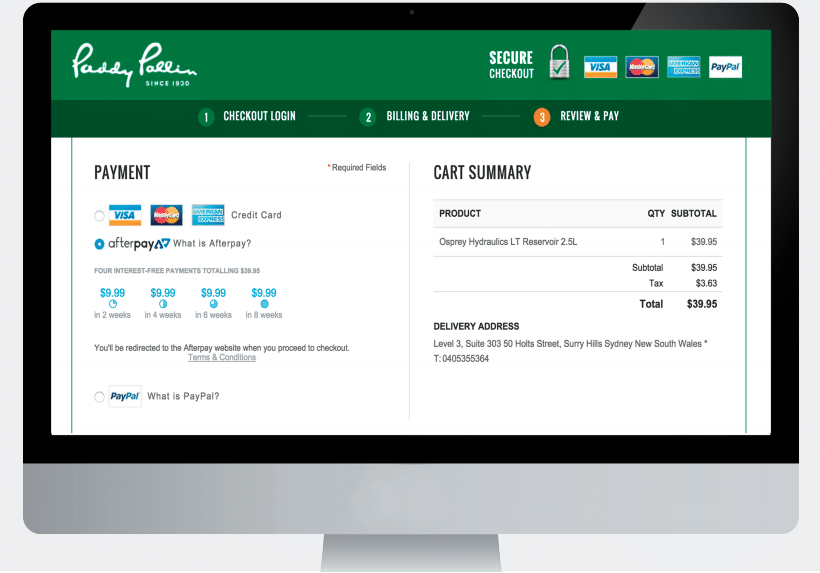

Afterpay Online

Here is a screenshot of how Afterpay works online:

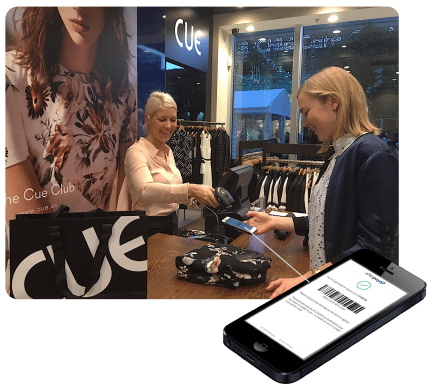

Afterpay Instore

Here is an example of how Afterpay works instore:

1.First you sign up at the checkout and receive a barcode:

2.The merchant then scans your barcode and your purchase is complete:

Why Are Businesses Using It?

Ever since the invention of the credit card in 1950, businesses have been searching for methods to get consumers to part with their hard earned cash.

Merchants (Businesses) want a sale so much they are willing to part with as much as 3% of the sale value in fees to credit card companies.

Afterpay is just another way for merchants to encourage you to buy today and once again they are prepared to pay Afterpay for this privilege.

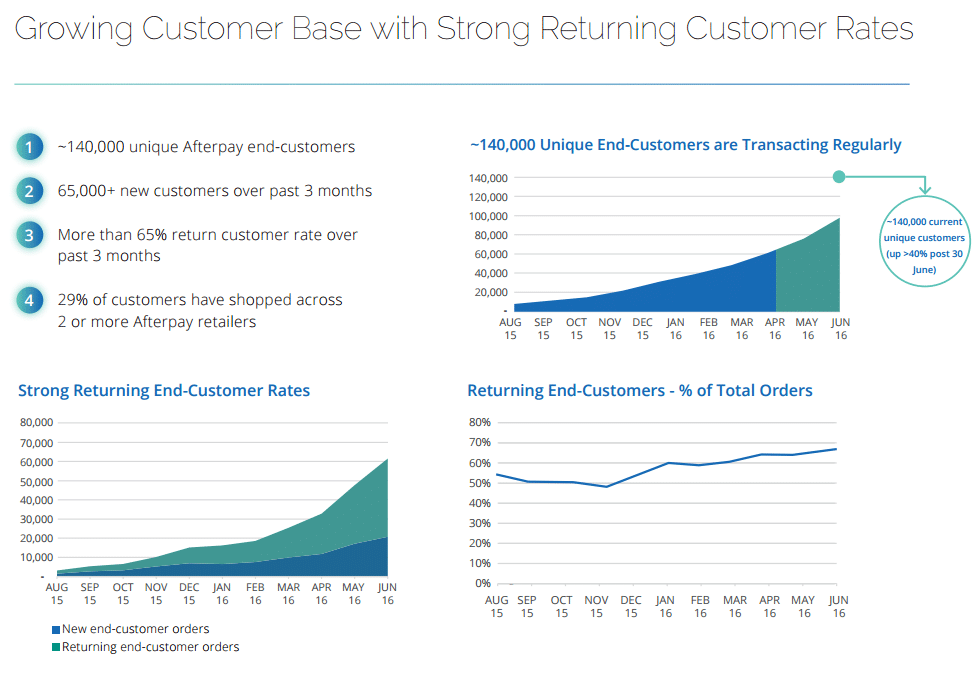

Early evidence from a number of businesses offering Afterpay, suggests that it does work to increase sales.

The evidence above shows:

- Afterpay users are up to 34% more likely to spend and

- Afterpay users will spend up to 25% more than the average customer.

This evidence has been enough to get merchants to sign up in droves.

What About Consumers?

Let’s face it, we all like to live in the moment and face the consequences tomorrow.

It will come as no surprise that customers love using Afterpay’s buy now, pay later offer.

- As at August 2016, 140,000 customers in Australia have used the Afterpay service

- 65% of Afterpay customers are repeat users

- As at August 2016, AfterPay was experiencing a net transaction loss rate of 0.9% – which means just under 1% of users were not completing their scheduled AfterPay repayments.

My Opinion of Afterpay

Afterpay is yet another way to buy now and pay later (or rather get it now and worry about the consequences later).

For

- If used with discipline you can get the product now and pay later, with no fees or interest.

- Unlike a credit card, AfterPay provides an automatic framework for repaying the amount in full

Against

- Encourages a ‘live in the moment’ mentality and can increase the tendency for impulse purchases

- You can pay the Afterpay instalments using a credit card, which has the potential to exacerbate potentially problematic credit card habits.

Verdict

Afterpay is a marketing method aimed at encouraging consumers to spend more now and worry about the consequences later.

Best Case Scenario:

Afterpay allows you to get the product you so desperately need now, and pay for it in regular instalments without paying interest or other fees.

Worst Case Scenario:

Afterpay allows you to purchase a product you don’t really need, in instalments on your credit card, which could further compound your already poor credit card habits (and the debt spiral associated with this).

The Final Word

Just like a credit card, Afterpay is a psychological play that has the potential to encourage impulse spending (after all that is why merchants are using it).

- If you ever experience periods of habitual overspending, you regularly pay interest on credit card purchases, or have other debt issues, you should probably steer clear of Afterpay.

- Afterpay is best used for purchases that you really can’t live without and paid off via your debit card not your credit card.

Have you started using Afterpay? Have you had a good or bad experience?

The information on this blog and website is of a general nature only. It does not take into account your individual financial situation, objectives or needs. You should consider your own financial position and requirements before making a decision. We recommend you consult a licensed financial adviser in order to assist you.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}