This comprehensive guide is here to help you understand how bridging loans work in Australia. To get free advice on whether bridging finance is right for you and the best products available – contact the Bridging loan expert Gerry Bosco on 1300 739 161 or email info@aplsfinance.com.au

A bridging loan is a loan facility which allows you to purchase a new home before you have sold your existing home with the intention of selling your existing home within a specified period of time.

It may be structured as two separate loans or some lenders join the loans together and use both securities as collateral. When the first home is finally sold, the proceeds go towards paying the loan down and the bridging period ends.

During the bridging period, interest only is usually paid or is capitalised and added to the loan at the end of the bridging period. In general, no actual principal repayments are made during this time. Although, there are some lenders that will allow principal repayments on the existing loan amount when kept separate.

Why would you get a bridging loan?

The purpose of a bridging loan is to assist you in purchasing a new home without the delays usually associated with selling your existing home acting as an obstacle. In the ideal scenario, you could sell your existing home & buy your next dream home with same day settlements. In reality though, this is extremely difficult to do due to the number of parties involved and trying to get the timing in sync with everyone.

In addition, if you have enough equity in your existing home, you can also add purchasing costs to the bridging loan such as stamp duty & legal fees.

How does a bridging loan work?

For a bridging loan to work, the lender needs to hold security for the existing property & the new one. As mentioned previously, this can either be as one total loan secured by both securities or as two separate loans. These two loans together are known as the ‘peak debt’ which means the highest debt this loan will have. Some lenders calculate serviceability based on peak debt.

There are also other lenders that calculate your serviceability based on ‘end debt’. This is the loan balance when you sell your first home (the sale amount is estimated at the time of the application) & pay down the peak debt with the sale proceeds. Obviously, this is a much more generous approach and borrowers will generally have a much better chance at passing servicing using this method. As the Royal Commission approaches its final report submission time early in 2019, it is likely many borrowers will not be able to extend their borrowing capacities sufficiently for the purpose of a bridging loan and thus the ‘end debt’ method will certainly be a welcome option for most.

Interest compounds monthly during the bridging period based on a pre-specific interest rate and is added to the balance at the end of the bridging period. This means that the longer you take to sell your home, the higher the compounded interest will be. In the early days of bridging loans, there were interest rate premiums during the bridging period, but in recent times these have largely gone and the rates now are much closer to discounted standard variable rates.

The bridging period typically lasts for about 6 months, though this can be longer by exception. That is, you are required to sell your first home during this time and use the proceeds to pay down the loan at which point the bridging period ends.

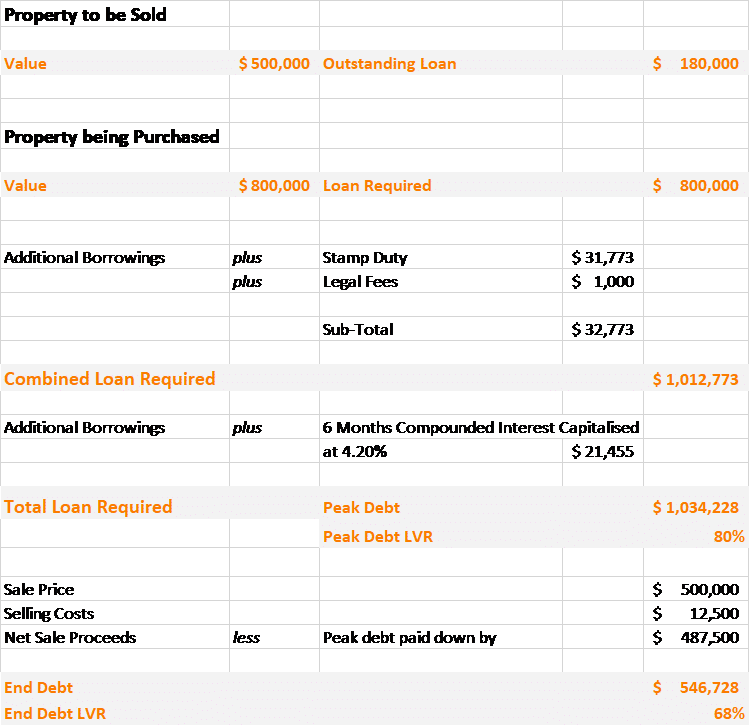

Case Study

Daniel & Katie had been planning on upgrading their home in recent years as their young family grew from two to four. Although, they didn’t expect they would have come across the home of their dreams so quickly.

Without enough time to sell their existing home in time to purchase their new home, they were able to use a bridging loan to buy the home of their dreams before selling their old home. This scenario assumes that their existing home is carrying some debt & they will borrow the full amount of the next home plus costs. Also, there will be an end debt. This is what the numbers looked like:

In the example above, the Daniel & Katie were able to go with a lender who uses ‘end debt’ to calculate their serviceability to push their capacity that little bit further. They needed to ensure their LVR at the peak debt was at or under 80% to avoid LMI as that was their preference. Their actual peak debt was $1,034,228. Upon selling their original home and using the net proceeds of $487,500 (after selling costs) to pay down the bridging loan, the end debt was reduced to $546,728 with an LVR of 68% signalling the end of the bridging loan process.

What are the risks of bridging loans?

There are some risks involved with bridging loans that borrowers need to be aware of. If these can be controlled, then the bridging loan process will be relatively smooth and hassle free. Your mortgage broker will still need to advise you on some of the potential risks of using a bridging loan.

One of the risks stems from having an emotional attachment to their previous home and believing it’s worth more than it is. This risk is not specific to bridging loans, but in general with selling a home. The significance here is that if the home isn’t sold within the 6 months bridging period, there may be costly consequences.

Firstly, the interest rate will likely increase, which is never a good thing & secondly, the loan may revert to principle & interest payments on the whole amount. This could lead to massive financial strain on borrowers who were not prepared. To combat this risk, it is important to ensure that the asking price be a realistic market supported price which should sell within the allocated time frame of the bridging loan.

Also, it should be noted that not all lenders offer bridging finance so if your current lender does not offer it, you may need to refinance to a lender that does. This may come at a significant cost if you’re on a fixed rate and really want to buy that dream home. It is important to be aware of your options and also the costs involved as early as possible to ensure you are making a cost effective and informed decision.

In summary, how can a bridging loan help me?

Bridging finance can provide some relief & ease some pressure of attempting to match up settlement dates if structured in the right way. It will also allow you to sell your existing home and secure your new one with a structured step by step approach.

As with all major financial decisions, there are risks therefore careful research using these research tools for example, and advice from your mortgage broker should be sought in order to minimise these risks where possible and be informed about the process & what is entailed as much as possible to ensure a smooth bridging process.

If you’re looking for a bridging loan – Gerry Bosco from Precision Funding Sydney can assist. An expert in bridging loans and facilities, Gerry helps borrowers across Australia purchase their next home across any scenario. Contact Gerry Today by calling 1300 739 161 or using our fast response contact form.

Leave A Comment

You must be logged in to post a comment.